If you have ₹5,000 sitting in your savings account every month, you are probably wondering: should I start a SIP in mutual funds, or simply put it in a Fixed Deposit? This is one of the most common financial dilemmas for Indians — and for good reason. Both options are popular, widely trusted, and easy to access. But they are built for completely different financial goals.

In this article, we break down SIP vs FD in simple language, with real numbers, so you can decide which one is right for you.

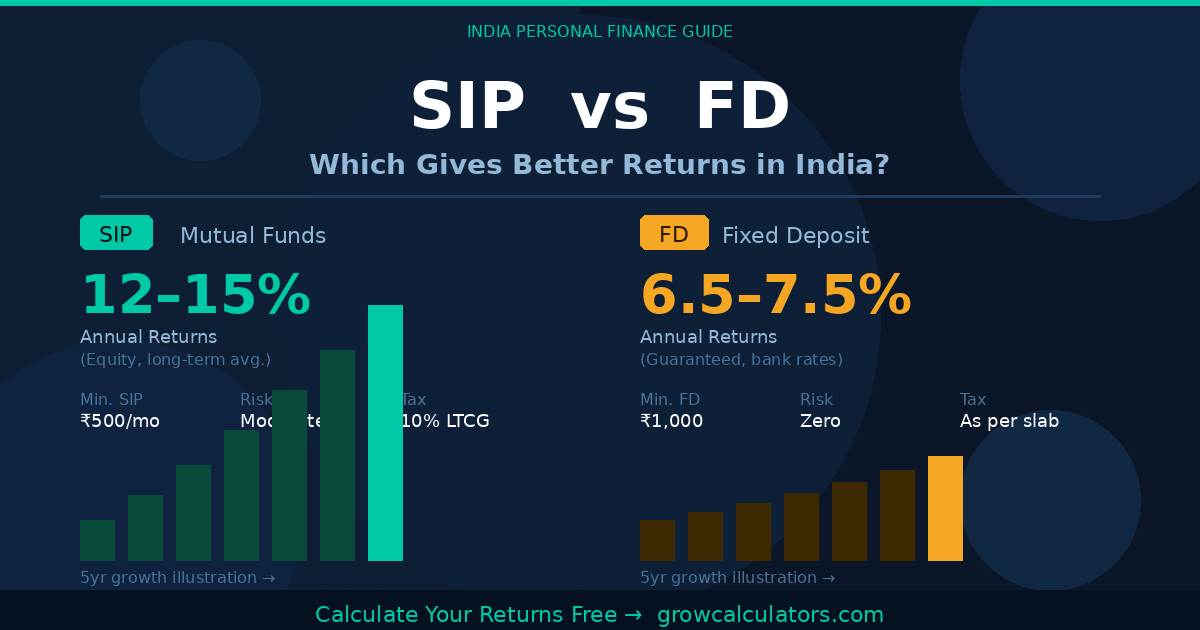

What is a SIP?

A Systematic Investment Plan (SIP) lets you invest a fixed amount every month into a mutual fund. The money gets invested automatically on a chosen date, buying mutual fund units at the prevailing market price. Over time, you benefit from rupee cost averaging — you buy more units when markets are low and fewer when markets are high.

SIPs are flexible — you can start with as little as ₹500 per month and stop, pause, or increase your amount anytime. Most equity mutual funds have historically delivered 10–15% annual returns over a 7–10 year horizon.

| 💡 Use our SIP Calculator at growcalculators.com to estimate how much your monthly SIP can grow over 10, 15, or 20 years. |

What is a Fixed Deposit (FD)?

A Fixed Deposit is a savings instrument offered by banks and NBFCs where you deposit a lump sum for a fixed tenure at a pre-agreed interest rate. The returns are guaranteed — regardless of what happens in the stock market.

Most major Indian banks currently offer FD interest rates between 6.5% and 7.5% per annum. Senior citizens typically get an additional 0.25–0.50% over regular rates.

| 💡 Want to see your FD maturity value in seconds? Use our FD Calculator to compare different tenures and interest rates. |

SIP vs FD – Side-by-Side Comparison

| Feature | SIP (Mutual Fund) | Fixed Deposit (FD) |

| Returns | 10–15% p.a. (equity) | 6.5–7.5% p.a. |

| Risk | Market-linked (moderate-high) | Guaranteed (no risk) |

| Minimum Investment | ₹500/month | ₹1,000 lump sum |

| Lock-in Period | None (ELSS: 3 years) | 7 days to 10 years |

| Liquidity | High (redeem anytime) | Penalty for early exit |

| Tax on Returns | LTCG 10% above ₹1 lakh | Taxed as per slab |

| Inflation Beating? | Yes (historically) | Often No |

| Best For | Long-term wealth creation | Capital preservation |

Real-World Examples: SIP vs FD with ₹5,000/month

Let’s take a practical scenario. Suppose Priya and Ravi both decide to invest ₹5,000 per month for 10 years. Priya puts her money in an FD (renewing annually at 7% p.a.). Ravi starts a SIP in a diversified equity mutual fund expecting 12% p.a. Who comes out ahead?

| Priya – FD (7% p.a.) | Ravi – SIP (12% p.a.) | |

| Monthly Investment | ₹5,000 | ₹5,000 |

| Tenure | 10 Years | 10 Years |

| Total Invested | ₹6,00,000 | ₹6,00,000 |

| Maturity Value | ~₹8,65,000 | ~₹11,62,000 |

| Gain | ~₹2,65,000 | ~₹5,62,000 |

Ravi’s SIP gave him almost double the gain compared to Priya’s FD — ₹5.62 lakh vs ₹2.65 lakh.

But here is the important caveat: Ravi’s returns are not guaranteed. In a bad market year, his returns could be lower. Priya’s ₹8.65 lakh is locked in regardless.

| 📊 Calculate your own SIP vs FD scenario using our free calculators and see the difference in black and white. |

Tax Treatment: SIP vs FD

Tax is a critical but often ignored factor when comparing SIP and FD returns.

Fixed Deposit Tax: FD interest is fully taxable as per your income tax slab. If you are in the 30% tax bracket, you effectively lose 30% of your FD earnings to tax. TDS is also deducted at 10% if your interest exceeds ₹40,000 in a year.

SIP Tax (Equity Funds): If you hold equity mutual fund units for more than 1 year, gains are classified as Long-Term Capital Gains (LTCG). You pay 10% tax only on gains exceeding ₹1 lakh in a financial year. This is significantly lower than FD tax for most investors.

| FD (7% pre-tax) | SIP Equity (12% assumed) | |

| Pre-tax Gain | ₹2,65,000 | ₹5,62,000 |

| Tax Paid | ~₹79,500 (30%) | ~₹46,200 (10% LTCG) |

| Post-Tax Gain | ~₹1,85,500 | ~₹5,15,800 |

The tax advantage makes SIP even more attractive for investors in higher tax brackets.

Who Should Choose SIP?

- You have a long-term investment horizon (5 years or more)

- You want to build wealth and beat inflation over time

- You can tolerate short-term market fluctuations

- You want to invest regularly without a large lump sum

- You are saving for goals like retirement, child’s education, or home purchase

Who Should Choose FD?

- You want guaranteed, risk-free returns

- You have a short-term goal (1–3 years)

- You are a senior citizen looking for steady income

- You cannot afford to lose your principal amount

- You are saving for an emergency fund or near-term expense

Can You Do Both SIP and FD?

Absolutely — and in fact, most financial advisors recommend a combination. Here is a simple framework:

| Investor Profile | SIP Allocation | FD/Debt Allocation |

| Young (20–30 years) | 80% | 20% |

| Mid-career (30–45 years) | 60–70% | 30–40% |

| Near Retirement (45–55 years) | 40–50% | 50–60% |

| Retired (55+ years) | 20–30% | 70–80% |

The idea is simple: use SIP for long-term wealth creation, and FD for capital protection and liquidity. Your emergency fund (3–6 months of expenses) should always be in FD or a liquid fund — never in equity SIPs.

The Inflation Factor: Why FD May Not Be Enough

India’s average inflation rate hovers around 5–6% per annum. When your FD gives 7% returns and inflation runs at 6%, your real return is just 1%. In some years with high inflation, your FD may not even cover the erosion in purchasing power.

Equity SIPs, over a long period, have consistently beaten inflation by a wide margin. The Nifty 50 index has delivered approximately 12–13% CAGR over the last 20 years — making it one of the best long-term inflation-beating instruments available to Indian retail investors.

| 📌 Use our Inflation Calculator at growcalculators.com to see how inflation affects your money’s real value over time. |

The Final Verdict: SIP vs FD

There is no universal winner between SIP and FD — the right choice depends on your goals, timeline, and risk appetite. Here is a quick rule of thumb:

- Need money within 1–3 years? → Go with FD.

- Investing for 5+ years? → SIP in equity funds will likely give you better returns.

- Want complete safety? → FD is your answer.

- Want to beat inflation and grow wealth? → SIP wins hands down.

The smartest approach is to not treat this as an either/or decision. Build a portfolio where FDs handle your short-term security and SIPs power your long-term wealth creation.

Calculate Your Returns Right Now

Ready to see the numbers for your specific investment? Use our free calculators at GrowCalculators.com:

- SIP Calculator – See how your monthly SIP grows over time

- FD Calculator – Calculate your Fixed Deposit maturity value

- SWP Calculator – Plan systematic withdrawals from your mutual fund

| ✅ All calculators are free, no sign-up required. Get instant results tailored to your investment inputs. |

Disclaimer: Mutual fund investments are subject to market risks. Past performance is not indicative of future results. FD interest rates are subject to change. Please consult a SEBI-registered financial advisor before making investment decisions.